Today we will start accounting information systems chapter. AIS Chapter 2 is about Transaction processing systems and its cycles. In the first chapter of the Accounting information system, we started with a basic definition of the accounting information system and elaborated the concepts of what is a system , what is an information system and then what are particularly accounting information systems. We discuss the sub system of accounting information systems and general framework of accounting information systems with the ending discussion evolution of accounting information systems.

What is transaction processing system (TPS)

One of the most fundamental and important subsystems of AIS. As we define it in our previous lecture, when we discussed the framework of AIS. This system(TPS) is responsible for converting financial events into . transactions. Recording of Transaction in Journals and vouchers and distributing necessary information for daily operations. examples of transaction processing systems in AIS are sales order entry, payroll, employee records, manufacturing, and shipping management systems.

Transaction processing system definition

In an Accounting information systems, TPS is the most fundamental system that is responsible for recording of Transaction in Journals and vouchers and distributing necessary information for daily operations.

Types of transaction processing system in AIS

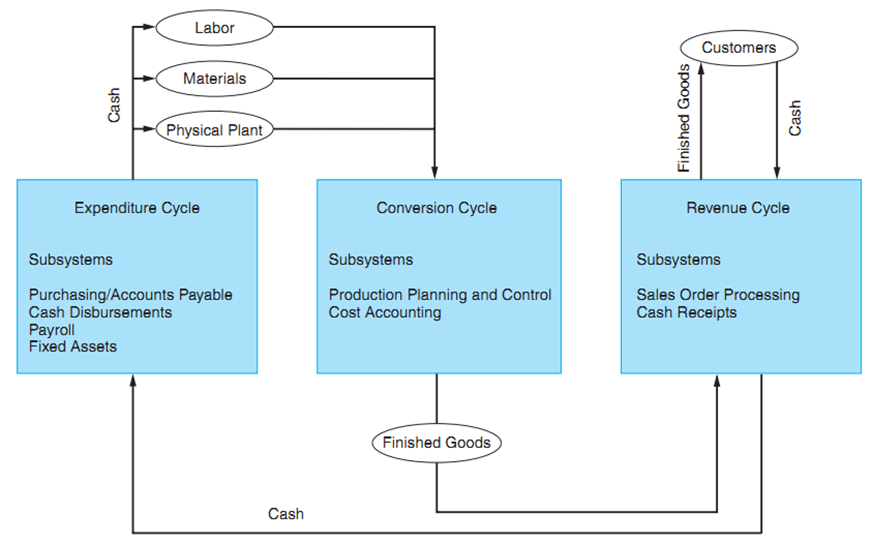

There are three main Subsystems of TPS including the revenue cycle, the expenditure Cycle and the conversion cycle. all of these cycles support different objectives. All of these have similar characteristics. For example, all three capture financial transactions, record the effects of transactions, and produce information about transactions to support day-to-day activities.

What is Transaction in TPS?

Let’s start with the definition of Transaction “ An economic event that affects the assets and equities of the firm, is reflected in its accounts, and is measured in monetary terms.” e.g. Sale of goods or services, the purchase of inventory, the discharge of financial obligations and the receipt of cash on account from customers. Financial transaction can initialized by internal events like the depreciation of fixed assets, the application of labor raw materials overhead to the production process, transfer of inventory from one department to another, There may thousands of transactions for a business in a day. The only way to handle these efficiently is to group them. Figure shows the relationship of these cycles and examples of all transactions processing systems in an AIS.

Expenditure Cycles

Every business starts with the purchase of materials, property, and labor in exchange for cash. Most expenditure transactions are based on a credit relationship between the trading parties. The actual disbursement of cash takes place at some point after the receipt of the goods or services.Thus, from a systems perspective, this transaction has two parts: a physical component (the acquisition of the goods) and a financial component (the cash disbursement to the supplier).

Subsystems of Expenditure Cycles

Purchases/accounts payable system. This system identifies the need to acquire physical inventory (such as raw materials) for example Places an order with the vendor. After receiving goods the purchases system records the event by increasing inventory and establishing an account payable to be paid at a later date.

Cash disbursements system is responsible for authorizing the payment, disburses the funds to the vendor and records the transaction by reducing the cash and accounts payable accounts.

Payroll system is another example of TPS that collects labor usage data for each employee, computes the payroll, and disburses paychecks to the employees.

Fixed asset system works with transactions involving the acquisition, maintenance, and disposal of its fixed assets. These are relatively permanent items that collectively often represent the organization’s largest financial investment. Examples of fixed assets include land, buildings, furniture, machinery, and motor vehicles.

The Conversion Cycle

The Conversion Cycle is composed of two major subsystems: the production system : activities?The production system involves the planning, scheduling, and control of the physical product through the manufacturing process, determining raw material requirements, authorizing the work to be performed and the release of raw materials into production.

The cost accounting system is major in this cycle and it monitors the flow of cost information related to production. It generated cost Information which is useful for inventory valuation, budgeting, cost control, performance reporting and management decisions.

The Revenue Cycle

Firms sell their finished goods to customers through the revenue cycle. All transactions that include cash sales and credit sales are recorded and processed by this cycle of TPS. Revenue cycle transactions also have a physical and a financial component, which are processed separately.

Sales order processing subsystem is responsible for preparing sales orders, granting credit, shipping products (or rendering of a ser-vice) to the customer and billing customers. Cash receipts. For credit sales, some period of time (days or weeks) passes between the point of sale and the receipt of cash.

Let’s Recap what we learned today in this lecture!

- Transactions

- Transaction Cycles

- Cash flow of TPS

- Subsystems of Cycles

- The Expenditure cycle

- Conversion cycle

- Revenue cycle